8 Things I Still Spend My Money On as a Millennial Girl on FIRE

/

The FI/RE community honestly gets a bad rap for being ultra-frugal, extremely thrifty, and a bit miserly for their spending habits, whether it's living out of a van or eating oatmeal for breakfast every single day. I'm here as a girl on FI/RE to show you that you don't have to live a life like that. There's a balance.

During this journey to financial independence, you should enjoy your life and live a life that is beautiful and meaningful to you. Spend on things that you truly believe in spending on. You can spend almost lavishly on things that bring you a lot of joy and you find meaningful to yourself.

So I wanted to talk to you guys today about the eight things that I still spend money on, even though I'm on my journey to early retirement and planning on retiring early at 35. I don't live a life of deprivation. I feel they don't, Brisbane who believes in being financially well and a part of that means spending money on things you truly love and care about.

1. I splurge a fancy gym membership

Something I prioritize is my health. The very first thing I spend money on is the gym. And not just any gym, I actually have an Equinox membership. Although since we're not able to work out in person, I put my membership on pause because what's the point of paying $200+ a month if I'm not able to go to the gym.

Under normal circumstances, I very much value spending on a nice luxury gym. The one I went to in Los Angeles has a saltwater lap pool. I love doing 30 minute swimming sessions. Plus they have great yoga classes and most importantly why I actually signed up, they have ballet classes at this gym.

I did ballet growing up and doing ballet now is something that gets me to move my body, but doesn't feel like exercise. It's great cardio when you're moving and jumping across the room, but you don’t think it’s a work out, it’s just dancing. I love that mind-trickery!

Not only that, but they have great yoga classes, sound baths, and meditations. Honestly, the steam rooms and saunas alone are worth it. And yes, those eucalyptus towels live up to the hype.

Again, it was about $200 a month—a slight discount through my work. Ultimately it keeps you in good shape and better health. Spending on things that will get me to move my body is worth it.

If you love running, I cannot stand it, but if you like those activities that are free, like, basketball or soccer or just do an at home Pilates workout, that is great for you. However, it's not what works for me. Spending money on a gym membership is 100% worth it.

2. I splurge on going out to eat

The next thing I always will spend money on is when a friend hangs out and asks to go out to eat. I'm always so down. I LOVE good food. LA has some of the best, most diverse, authentic food in a 10 mile radius. I'm always willing to go out to dinner with friends.

If I’m alone, I really try to not eat out. I don't typically pick up food for myself. Eating and dining out is more of an experience that I'm able to share with friends, share a meal with friends and try the delicious food in the city.

It's important to recognize if dining out is a crutch because you don't want to cook your food at home or is it an experience? Is it a meaningful time you are getting together with friends or is there an underlying issue with eating food at home?

Coffee also falls under this same category. I don't usually get coffee on myself unless I have a gift card or if a friend wants to meet up. Honestly, my cold brew and Oatly are as delicious as a latte out! However, hanging out with friends and having a shared experience over a meal is always worth it to me.

3. I still splurge on a new car

Something that is a shocker and goes against so many FIRE “rules” is getting a brand new car, straight from the dealership car.

I have had 3 cars in my life. Two were used CR-Vs—one was my dad's and the second was my uncle's. When it was finally time for me to buy a car on my own and hand down my old CR-V to my little sister, I got a brand new one.

I've had friends who have bought second hand and it turned out that their cars were lemons. They had undisclosed accidents and missing parts even though it was certified pre-owned. Because of that, I'm hesitant to get a car from people I don’t know directly. I'm not opposed to getting second hand cars, but for me personally, when buying a car for myself, I chose to buy a new.

4. I splurge on brand name clothing

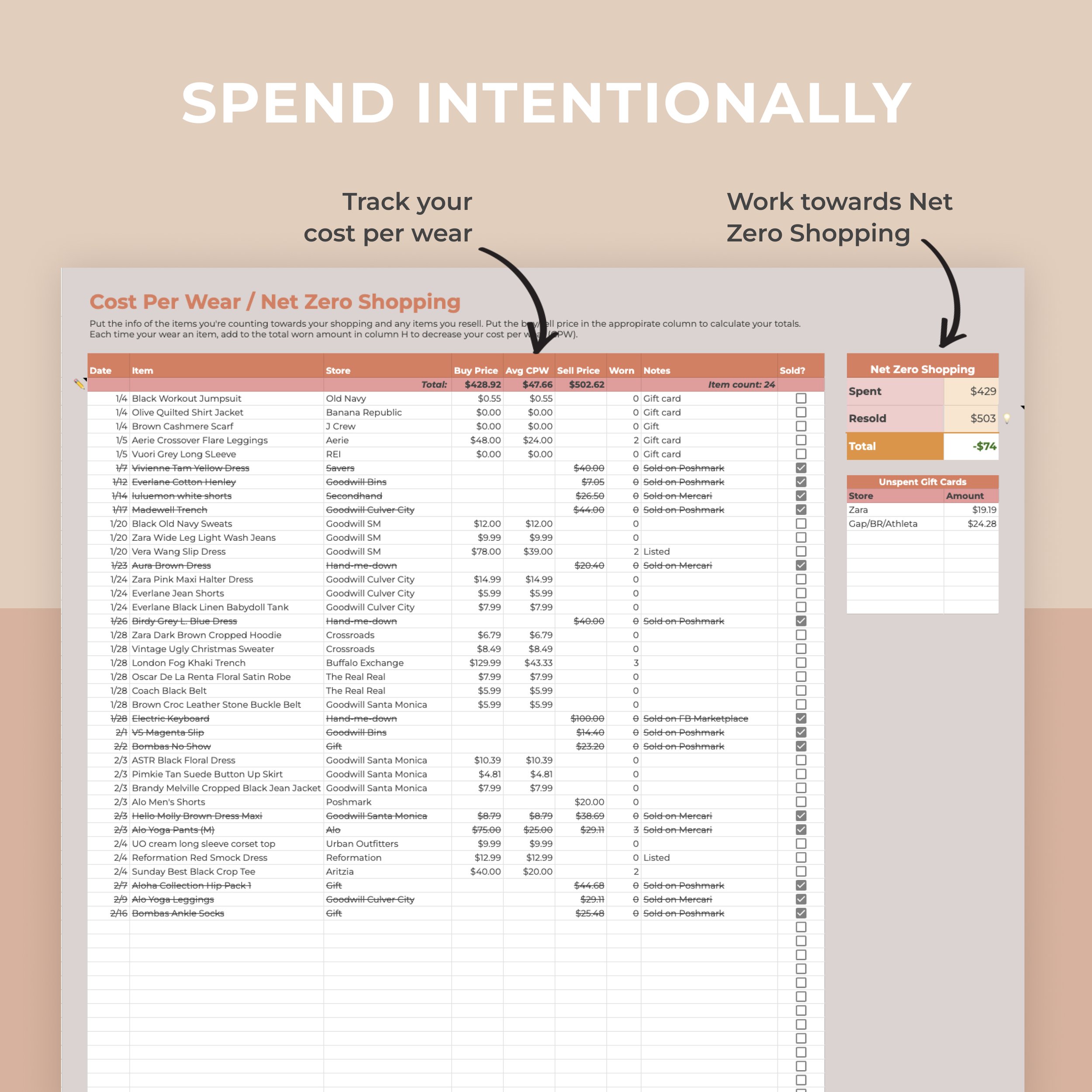

The next thing that I'm willing to spend money on is brand name clothing. The association with people on FIRE is that they dress poorly and don’t buy nice designer pieces. No, it’s not that I don't buy designer, I just don’t pay the full marked up price. I wear a lot of designer clothes and brand name clothes, I just get them secondhand. That’s the difference!

I'm willing to spend on quality secondhand pieces which is good from a financial perspective, but also from a minimalist and sustainability perspective. I want to reduce my carbon footprint and that is something that aligns with my values.

It's not that I'm not willing to spend money, I'm just not willing to spend money on new things that are perfectly fine secondhand. And I actually love going thrifting—it’s the thrill of the hunt. I got a Chloe jacket for $80 and I've gotten some other really good funds for much, much less than what they're worth.

5. I splurge on nice vacations

The next thing that I loved spending on is travel. It's been a year of being stuck inside, so I haven't done any major traveling lately. But the last trip I went on was to Japan and my gosh, we balled out. We ate lavishly, dropped hundreds on nice omakase style dinners and tried cocktails at every town we stayed in. We stayed at a really nice ryokan in Hakone. It was a magical experience. It was so serene, so beautiful.

The ryokan (Yamanochaya) we stayed at was in the woods. From areas around the lake you could see Mount Fuji in the background. (Although it was cloudy then when we went, so we actually didn't see it, but theoretically, you could.) And we had our own private, hot spring onsen inside our room. They served kaiseki meals, which is like omakase, but with more seasonal dishes. It was so beautiful and delicious. I loved the whole experience.

When it comes to travel, it's like, when are you going back to this place next? Those experiences are worth paying for in that moment. When I travel, I try to not think about the expenses and just enjoy those moments. It’s important to build those memories, take those photos and have those experiences that I will carry with me for the rest of my life.

6. I splurge on my hobbies

The next thing that I spend money on is this hobby of mine. This is truly a passion project and hobby of mine that I have so much fun doing, and I want to grow it and make it bigger and better.

So far, I’ve spent about $500, between my website, SEO optimization tools, and my YouTube gear. I use my iPhone 12 Pro to film, but I have a microphone, LED light, and things like that. It's definitely something I'm willing to spend money on because I love doing it.

I'm always willing to spend money on my hobbies that I truly enjoy. Whether it's hair bow making at the time or doing this YouTube.

7. I splurge on books

This goes hand in hand with spending on my hobbies. I'm very willing to spend money on books and education. In some sense, it's an investment in myself. Reading truly takes you to a new world! It's almost like a cheap vacation. It allows you to experience and empathize with characters or people who are outside of your little world.

Fiction books are great for that, but non-fiction expands your mind too. I love reading books about personal finance (obviously) and psychology. It all relates back to becoming a better person and that is absolutely always worth spending on.

For some reason, this does not translate for me to e-courses as much. Between Google and YouTube, those are such great resources for learning how to do basically anything. I haven't ever spent any money on e-courses, but let me know in the comments below, if you have and if you thought it was worth it.

For me, it's really hard to trust whether or not paying a person thousands of dollars is really going to teach me how to grow my YouTube channel better than just watching videos on the subject for free. This is why I put out all of my educational content for free and don’t have people buy any of this FI/RE finance information. I learned from the internet and you can too. That's my philosophy. Books, I'm a 100% willing to spend on. “Educational” e-courses I'm on the fence about—not going to lie. That's my personal opinion.

8. I splurge on celebrations

Lastly, I always spend money on celebrating the wins. I'm a huge believer in, making life a party. I took myself out to an omakase dinner last night because my contract got extended and I wasn’t sure if it was going to be. Last minute they were like, yeah, you got extended. You're doing such a great job!

That was such a big win for me. It means I can max out my 401k for the year. So I went out to celebrate and for me, celebrating can be something as simple as that. Honestly I think those wins are not celebrated enough, but when it's my birthday, I always celebrate another year of life! I will spend lavishly on hosting a party for my friends and the people that I care about because they are on this exciting journey of life with me.

When I retire early, I'm going to throw a giant party and YOU are invited. I want to have an awesome retirement party because that will be such a huge accomplishment to be financially independent! I’m so excited to celebrate this milestone.

Getting married I don't think is really a huge accomplishment anymore, but I do want to celebrate moments in life that are really meaningful. That will probably mean me spending on a wedding because it’s in line with who I am and what I value.

Even if other finance people say, well, that $30,000 could turn into $1 million dollars by the time you're 85, I’ll still probably do it. Yes, it could. But also it’s important to spend on things that align with your values now. It’s important not to look at it as a tradeoff if it’s something you truly love and care about and if it's something you can afford.

Thoughts & Reflections

These are the 8 things I'm willing to spend money on. It’s important to start thinking about how what you spend on aligns to your own values. That is the key to becoming really intentional with your spending. Check out my blog on value-based spending if you need more clarity into what you find meaningful to spend money on.

If you are also on your journey to FI/RE, let me know what you still splurge on in the comments below! I think it’s important to talk about and show others that it's okay to spend money on things you love and care about. And if you’re not already subscribed, be sure to subscribe to my YouTube channel below so we can spread the FIRE.

Let's retire early together!

Disclosure: Some links are affiliate links, meaning, at no additional cost to you, I may earn some compensation. All opinions are 100% my own! I truly appreciate you and your support. :)